The first question I was asked was whether I was consuming or saving myself. I answered that I was "cautiously" coming back into circulation like many others in the economy. Several of the answers I gave in the interview were, at least partly, based on the Amarach opinion surveys commissioned by the Department of Health, that I have been involved in designing and are available here. These surveys, along with several other studies, conducted through the covid period in Ireland, reveal a high degree of adherence to public health guidelines and strong support for restrictions. In general, the public has either been in favour of the level of restrictions or in favour of greater degrees of restrictions. While highly visible instances of people going against the letter or spirit of public health guidelines are likely to get media attention, a wide range of survey and mobility data suggests very high rates of compliance, and the survey data, in general, suggests high rates of risk aversion with regard to the virus.

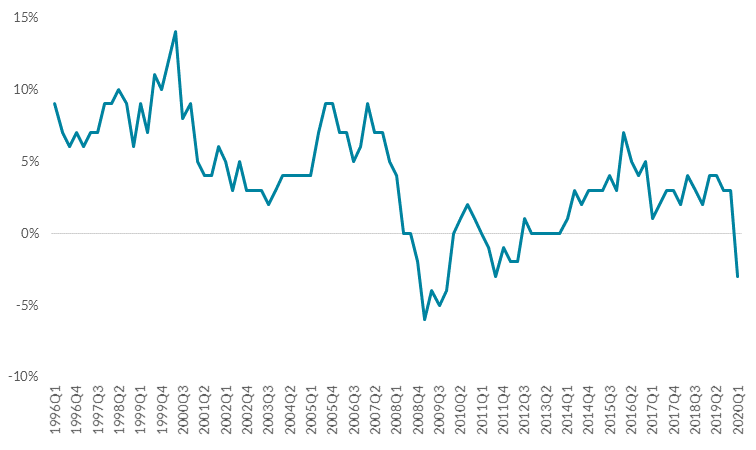

Related to this, a second thread of the interview related to declines in consumption and increases in deposits in the Irish context over the covid period. For background on this question, it is worth considering a number of recent documents. A particularly useful overview comes from Gabriel Maklouf, the Irish central bank governor, who discusses recent trends in Irish consumption in a recent speech available here. One key image from the speech is below, based on CSO data, showing the sharp decline in consumption arising since the start of covid. As discussed in the interview and in Governor Maklouf's speech, there are several potential reasons to expect a decline in expenditure. One reason is clearly enforced savings, with many regular types of consumption now being temporarily unavailable. Another is a variant of something we often see in the retirement literature, namely that much of the expenditure we see among people in the labour force relate to things like commuting, hotel accommodation, prepared food, etc., that simply don't need to be incurred when one is furloughed or working from home. The fall in expenditure we often see at retirement was basically extended over hundreds of thousands of workers simultaneously.

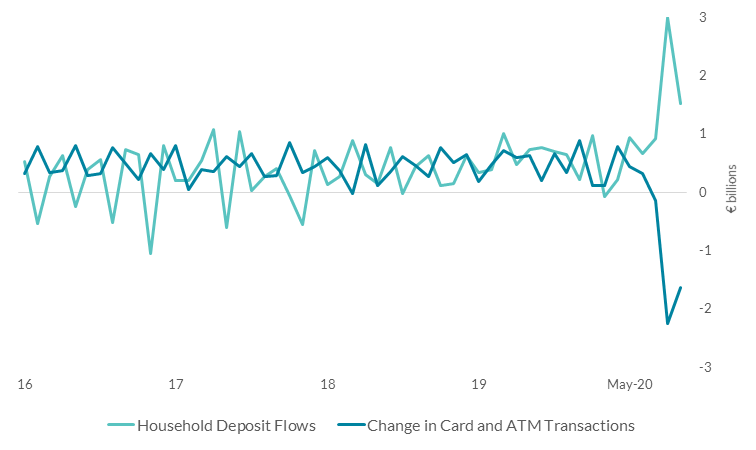

Relatedly, the last few months have seen a dramatic increase in deposits in Irish banks, as illustrated below by the graph from Governor Maklouf's speech. As discussed above, there are many reasons why one might expect a fall in expenditure and these could account for some of this deposit growth. Furthermore, there have been payment breaks on billions of euro of loans, some of which may reflect precautionary behaviour on behalf of workers worried about their labour market security. I referred to potential precautionary effects in the interview and also the possibility that a pattern of highly financially secure households increasing savings during periods of economic uncertainty may also be accounting for some of the deposit growth. The increase in deposits achieves something that many policies in Ireland have failed to achieve over decades, namely increasing the savings rate. However, it potentially comes at the cost of a slowdown in activity in sectors already very hit by covid and with potential employment effects. Furthermore, it is highly likely that the increase in deposits may have come from groups already in reasonable financial situations, something borne out by the CSO surveys. There is a lot more research needed on this but a combination of the various reports from ESRI, CSO, and Central Bank, paints a picture of covid having a disproportionate economic effect on low-to-middle income workers in affected areas such as hospitality and tourism and it is difficult to think that the deposit data reflects a deviation from these tendencies.

I was asked about the potential for recovery after covid in terms of the build-up of savings leading to increased consumption later in the process. I obviously do not have any particular forecasting powers in this area but it is plausible to think that the build-up of deposits could lead to a rebound in consumption in a covid-free environment and this has been discussed in a number of recent works by the ESRI and Central Bank as well as other commentators on such scenarios. But I did make the point that the very high degree of risk aversion emerging from most data sources suggests this is not something that will happen quickly. An interesting question arose in the interview as to whether norms of responsible behaviour might drive recovery in consumption to some extent. I think it would be worth thinking about this a lot more, particularly if a large amount of this deposit build-up comes from older financially comfortable households, who are considering whether it is appropriate to engage in different types of consumption activity. The extent to which the behaviour of such households might be affected by things like tax rebates for domestic expenditure is worth questioning, particularly policies like offering rebates where deadweight loss and administrative burden might detract from notional stimulus effects. I mentioned in the interview that thinking about different types of safety assurance systems might be a more promising way of sustainably increasing consumption in affected sectors such as hospitality. More generally, the Irish govt stimulus programme is focused mostly on bolstering the continuity of businesses and employment throughout the period of covid uncertainty and this seems like a more reasonable aim than attempts to directly stimulate expenditure in specific areas through rebates. This was discussed in detail at a recent Oireachtas committee session.

Notes:

I mentioned briefly the potential role of narratives in shaping responses to crises. The recent Princeton University Press book "Narrative Economics: How Stories Go Viral and Drive Major Economic Events" by Nobel Laureate Robert Shiller is a fascinating account of this and very relevant to the current situation.

I am member of the Central Bank Consumer Advisory Group and the NPHET behavioural change subgroup and have been thinking about these issues a lot over the last few months. Obviously, all thoughts offered here are given in a personal capacity.

The CSO social surveys are a very useful account of the social and economic impacts of covid on Irish households. The ESRI work on the employment and distributional consequences of covid are also very useful references. The IFS in London have also produced a remarkable set of reports on the economic impacts of covid, many of which are highly relevant in the Irish context.

A useful background reference is the research conducted by the Irish Competitiveness and Consumer Protection Council on health of household finances in Ireland.

Notes:

I mentioned briefly the potential role of narratives in shaping responses to crises. The recent Princeton University Press book "Narrative Economics: How Stories Go Viral and Drive Major Economic Events" by Nobel Laureate Robert Shiller is a fascinating account of this and very relevant to the current situation.

I am member of the Central Bank Consumer Advisory Group and the NPHET behavioural change subgroup and have been thinking about these issues a lot over the last few months. Obviously, all thoughts offered here are given in a personal capacity.

The CSO social surveys are a very useful account of the social and economic impacts of covid on Irish households. The ESRI work on the employment and distributional consequences of covid are also very useful references. The IFS in London have also produced a remarkable set of reports on the economic impacts of covid, many of which are highly relevant in the Irish context.

A useful background reference is the research conducted by the Irish Competitiveness and Consumer Protection Council on health of household finances in Ireland.

No comments:

Post a Comment